- Everyone Needs a Little Foresight

- (484) 368-3183

STANDARD MILEAGE RATES ARE GOING UP

December 20, 2017

IRS PROVIDES GUIDANCE ON 2017 DEDUCTIBILITY OF PREPAYING YOUR 2018 PROPERTY TAXES

December 28, 2017

THE TAX CUTS AND JOBS ACT

The 1,000 page tax reform bill “The Tax Cuts and Jobs Act” has been signed by President Trump. The new law will have vast changes to both individual and business taxation.

Below we summarized some of the key sweeping changes in the bill that will impact taxpayers:

INDIVIDUAL TAXATION:

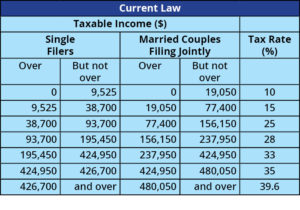

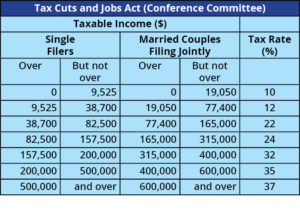

Tax Rate Change > Below are the 2018 tax brackets (under the current law and the Tax Cuts and Jobs Act):

Note > The capital gain and dividend rates are maintained at 0%, 15% and 20% brackets, plus the 3.8% surtax, where applicable. The rates are set to expire after year 2025 and if not renewed by congress the current tax law rates will tax effect with tax year 2026.

Standard Deduction Increase > Increases the standard deduction to $12,000 for single filers, $18,000 for heads of household, and $24,000 for joint filers in 2018 (compared to $6,500, $9,550, and $13,000 respectively under current law).

Personal exemptions are gone > these have been repealed and merged in with the higher standard deduction.

Child Tax Credit Increase > The Child/Dependent Tax Credit will be $2,000 with $1,400 refundable. Modified income limits (more people will be able to claim this credit) will make the credit available to more families and a $500 credit will be available for a non-child dependent.

Alternative Minimum Tax > The act retains a modified Individual Alternative Minimum Tax (AMT) as of 2018 and provides for increased exemptions and higher phase out limitations. The limits are indexed for inflation. The new law will change the impact of AMT and should reduce the number of affected taxpayers.

Itemized Deductions > There are significant changes to itemized deductions. The “Pease” limitation, which previously limited up to 80% of most itemized deductions, has been repealed. Instead, most itemized deductions are either eliminated or modified, such as:

- The deduction for non-business state and local income, sales and property taxes will be limited to $10,000 in aggregate ($5,000 for married taxpayers filing separately). This provision potentially harms taxpayers living in high income and property tax states.

- The deduction for medical expenses has been retained and will be enhanced. The act lowers the threshold for the deduction to 7.5% from 10% of adjusted gross income for tax years 2017 and 2018.

- The act repeals all miscellaneous itemized deductions that were previously subject to the 2% floor. Miscellaneous deductions included investment fees, tax preparation expenses and unreimbursed employee business expenses. However, the deduction for investment interest expense remains unchanged.

- The deduction for personal casualty and theft losses is repealed, except for losses resulting from federally declared disasters.

- The adjusted gross income limit on cash contributions is increased from 50% to 60%.

- 529 Savings Plans can be withdrawn tax-free if used for higher education expenses. The act now allows up to $10,000 per year to be used for elementary and high school tuition and funds to be used for private and religious schools.

- The deduction for mortgage interest is subject to the following rules:

- Interest on acquisition debt currently in existence can be deducted under current rules.

- The $1 million debt limit is reduced to $750,000 for debt incurred after December 15, 2017, and will only include mortgage interest deduction on a principal residence and second residence.

- Home equity interest will be nondeductible.

Individual Health Insurance Mandate > The final act includes a repeal of the Shared Responsibility Payment Penalty under the Affordable Care Act after 2018. Credits and Other

Adjustments to Income Changes > The act eliminates many tax credits and income exclusions, including (but not all inclusive):

- Moving expenses other than those in Armed Forces.

- Deduction or alimony payments effective for any divorce decree or separation agreement executed or modified after 2018.

- Elimination of the Deduction for Domestic Production Activities (DPAD).

Foresight Year-End Planning Tips:

- Make sure you pay your state and local income tax 4Q estimated tax payments before December 31, 2017. Or if you think you may have to pay in with your 2017 state or local income tax returns, consider making a 4Q estimated payment for the expected balance. In 2018, there is a limit to your total state, local and real estate taxes (there is no limit in 2017). You are not allowed to ‘Pre-pay’ your 2018 state and local taxes. Note > for tax payers in AMT in 2017, this strategy may not benefit you.

- Consider pre-paying your real estate / property taxes that are due in 2018. Unlike the state and local taxes, there is not yet specific guidance on whether or not the IRS will disallow these prepayments on your 2017 tax filings.

- For tax payers that will convert to the higher standard deductions, it may not be beneficial for you to itemize you deductions anymore in 2018 and beyond. Therefore, you should consider making early donations (cash or non-cash) in tax year 2017 so you will get a tax benefit on them in 2017. In addition, charitable donations (cash or non-cash) could be worth more in 2017 instead of 2018 due to the change in the rates.

- Miscellaneous itemized deductions such as tax prep fees and investment advisory fees are disallowed after tax year 2017. Therefore, if you can claim those deductions and get a benefit in tax year 2017, you may want to prepay your tax prep fee and also pay the 1st quarter of your investment advisory fees (talk to your financial planner about any compliance concerns with this recommendation).

- Pre-paying your January 2018 mortgage payment (part of that payment will be December 2017 interest expense).

- Employee Withholding at work > Make sure you work with your employer to update your work withholding in 2018. Here is a recent statement from the IRS: We anticipate issuing the initial withholding guidance (Notice 1036) in January reflecting the new legislation, which would allow taxpayers to begin seeing the benefits of the change as early as February. The IRS will be working closely with the nation’s payroll and tax professional community during this process

PASS THRU ENTITY TAXATION (SCORP, PARTNERSHIPS, SOLE PROPS)

- An individual taxpayer may deduct 20% of domestic qualified business income from partnership, S corporation or sole proprietorship.

- The amount of the deduction will be limited to the greater of:

- 50% of W-2 wages paid by the business or;

- The sum of 25% of W-2 wages paid by the business and 2.5% of business capital.

- The wage limitation does not apply if taxable income is less than $157,500 (single) or $315,000 (joint) and applies fully if taxable income exceeds $207,000 (single) or $415,000 (joint).

- Trusts and estates will qualify for this deduction.

- The deduction is a post adjusted gross income item.

- The deduction is not affected by whether the owner is passive or active.

- For specific service businesses, such as those in accounting, law, consulting, and investing, but not engineering or architecture, the 20% deduction will apply only if the taxpayer’s taxable income is less than $157,500 (single) or $315,000 (joint). No deduction will be allowed if the taxable income exceeds $207,000 (single) or $415,000 (joint).

- The act changes the long-term capital gains holding period for certain assets held in partnerships engaged in investment and real estate activities (carried interest). After 2017, a three year holding period is created for long-term capital gain treatment of gains for a carried interest (instead of the typical one year requirement).

Foresight Year-End Planning Tips:

- For qualified and eligible small business owners this is a huge win for 2018 and beyond. Therefore, business owners should consider deferring income to tax year 2018 by using some of the following tips:

- Slow down your year-end billing so that customer payments are received in tax year 2018. Note > you cannot hold deposits received in tax year 2017.

- Making purchases that were planned in the near future (assets, tools, repairs)

- Pre-paying certain expenses due in January or early 2018

- Paying year-end bonuses in 2017 vs 1Q 2018

BUSINESS TAXATION

- Lower the top corporate tax rate from 35% to a flat 21% (the same flat rate applies to personal service corporations).

- Allows immediate expensing of 100% of the cost of new investments in depreciable assets acquired after September 27, 2017, and before January 1, 2023. (The placed-in-service date will be extended for one year for property with a longer production period).

- Unlike the present bonus depreciation rules, the asset does not have to be new property; however, it must be the business taxpayer’s first use of such property.

- Qualified property does not include any property used in a real property trade or business.

- Section 179 expensing is increased to $1 million for years 2018 to 2022. A phase-out of the Section 179 benefit will begin when the purchases exceed $2.5 million. (Qualified energy efficient heating and air conditioning property will be included as Section 179 property).

- Caps will be placed on write offs of business use vehicles. The new caps will be $10,000 for the first year a vehicle is placed into service, (presently, $3,160).

- Eliminate the deduction under Internal Revenue Code § 199 for domestic production (DPAD).

- Net Operating Losses (NOLs) would generally not be eligible for a carryback. However, any carryover can be used only to the extent of 80% of taxable income. This rule will apply to losses arising in tax years beginning after December 31, 2017. Additionally, the carryforward period will be indefinite.

- No deduction will be allowed for entertainment, amusement or recreation activities facilities, or membership dues relating to such activities or other social purposes. However the current deduction for business meals (subject to the 50% limitation) will be retained.

- Section 162(m) related to limitations on deductions for compensation to executives has been modified. The exception to the $1 million compensation limit for executives of publicly traded companies for commission and performance-based compensation, will be repealed effective for years beginning after December 31, 2017.

- Corporations and partnerships with corporate partners with average gross receipts of up to $25 million (indexed for inflation) are allowed to use the cash method of accounting. Existing corporation that meet this gross receipts threshold can automatically change their accounting method.

CONCLUSION

There are many more changes to both individual and business taxation not mentioned above. There are also sweeping changes to Estates, Trusts and International tax provisions that we did not cover. Remember this is a 1,000 plus tax bill. We expect future clarifications to the Tax Cuts and Job Act bill in the near future and if noteworthy we will keep you posted.

Of course, everyone’s tax situation is different. Please contact us with any further questions. As part of preparing your 2017 taxes this year we will also discuss the new tax law and how it will impact your specific tax situation.